November 9, 2017

L&S Risk Pulse™ Score

Medium +

Core economic indicators are healthy, but markets indicate potential near-term volatility and/or mild correction. Valuations are trending high.

L&S Risk Pulse™ Insights – “Why is the Market Up When Our Political System is Falling Down?”

General Comments

The S&P 500 is up dramatically since the election of Donald J. Trump one year ago, yet many people feel a sense of dread about the prospects for our democracy. That palpable sense of dread is not just prevalent among those who did not vote for Mr. Trump, but also among those who are disappointed that the infighting within the Republican party has prevented significant legislative accomplishments. Prospects for the corporate tax cut seem difficult because the plan calls for elimination of the deductibility of state and local taxes, and for a smaller mortgage interest deduction. The elimination of these benefits is putting pressure on Republicans elected in strongly blue states to disavow the plan. We suspect that the probability of success for the tax cut plan are no better than 50/50 as it is currently written. Following the inability of the Republicans to repeal and replace Obamacare, another legislative failure could be damaging to their mid-term prospects.

There are two good reasons why the market is going up when our political system seems to be in disarray. The first answer is that very little of a presidential candidate’s agenda ever gets passed into law. A JPMorgan study showed that since Nixon, only about 9% of the pre-election agenda ever makes it into legislation. If you don’t like the agenda, fear not because only a modest amount of it is likely to come to fruition. If you do like the agenda, take solace in your victory even as very little is likely to get done.

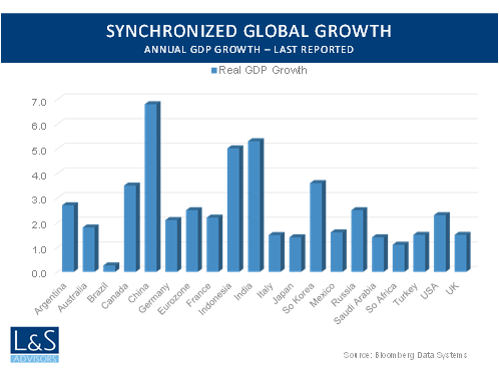

The second, and most important reason why the market is going up is the simple fact that global economic growth is solid. For the first time since the end of the Great Recession we have synchronized global growth. Even beleaguered Brazil is growing after years of being mired in a serious recession. The chart below shows that all 20 of the G-20 nations are growing. We are witnessing global synchronized growth, and with strong economic growth comes strong corporate earnings, and that leads to higher stock prices. In many ways, the stock market is ignoring the political ineptitude and is properly focused on strong economic growth.

Data Points and Global Economic Indicators

We look for risk every day, every week, every month. It is not that we are morbidly hoping for a catastrophe. It is simply that we do not want to be blind to a looming problem. We see this as one of the things that differentiates us from other firms. Our L&S Risk Pulse™ is a qualitative summary of the risk data we collect each period. Yes, we acknowledge that valuations are somewhat extended.

Further, we recognize that this has been one of the longest expansions in history. Still, we are hard-pressed to find data that suggests a pending end to the current expansion.

We do not want to see a border adjustment tax, or a trade war, or tariffs on imported goods. These things would likely slow growth, reduce earnings, and lower stock prices. Further, we do not want to see the Fed err by raising interest rates too aggressively. The recent appointment of Jerome Powell as Chair of the Fed suggests that the current

monetary policy will remain unchanged. We expect some regular but modest interest rate increases, but we do not see the makings of a policy error that would put the current expansion in jeopardy.

Conclusion

We remain cautiously optimistic regarding the prospects for continued economic growth. The fact that some people are dissatisfied with the current political paralysis is not a good thing. So far, that negativity has not had a deleterious impact on consumer, small business, or corporate confidence. We will continue to look for signs that confidence is being eroded in a meaningful way. Until the data suggests otherwise, we will continue to be fairly fully invested in the sectors that we feel will best participate in the global economic growth currently occurring.