July 13, 2017

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate.

— U.S. Federal Open Market Committee, June 14, 2017

All the signs now point to a strengthening and broadening recovery in the euro area…As the economy continues to recover…the central bank can accompany the recovery by adjusting the parameters of its policy instrument.

—European Central Bank President Mario Draghi June 27, 2017

Some removal of monetary stimulus is likely to become necessary.

— Bank of England Governor Mark Carney, June 28, 2017

The stock market appears to have gone through two transitions in the first half of this year. As the year began, the market seemed enamored with potential growth initiatives that would come from the newly-elected Trump administration. Lower regulation, lower taxes, infrastructure spending, and a revitalized healthcare plan were the election promises that the market fully embraced from the morning following the election. Those promises would result in faster growth, and combined with reduced taxes, would generate substantial growth in corporate profitability. The market loved the prospects.

Something happened as the replacement for Obamacare was put in front of the House of Representatives. They could not initially pass the bill, and the legislation was pulled before an embarrassing vote could be concluded. With the initial failure of the healthcare bill, the market perceived that the prospects for the entire Trump agenda were now in jeopardy. After all, if the GOP could not pass their signature legislation, what would happen to the other aspects of the platform? The perception was that the best case for the rest of the legislation would be a delay until perhaps 2018, with more dire consequences suggesting that all of the President’s pet projects would meet a fate similar to the healthcare plan.

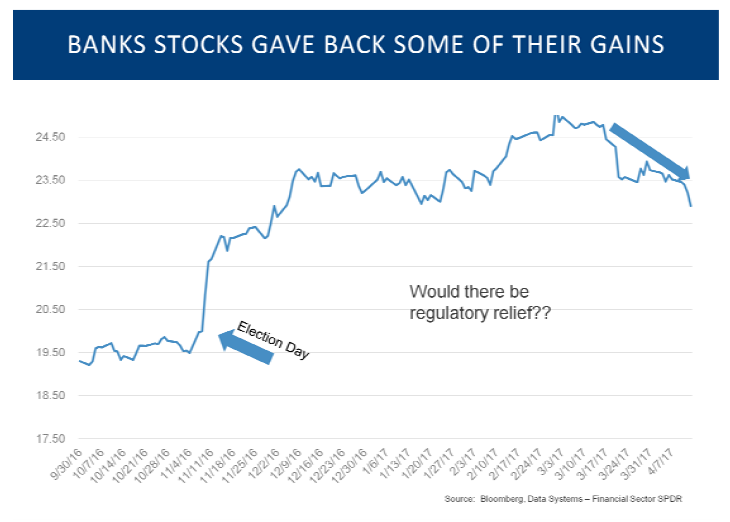

As the prospects for postponement of reduced regulation became a reality, the bank stocks, which had been one of the strongest post-election performers, started to correct. So too did commodity stocks that would have been the beneficiaries of increased materials purchases for infrastructure projects. The post-election rally seemed to be playing in reverse.

The market started to hunt for new leadership, but it was hard to figure out where we were in the economic cycle and what sectors should be preferred. The technology stocks emerged as one of the few leaders based on the idea that these stocks could deliver growth even if the economy was only plodding along.

Then the second market transition occurred. Prospects for growth continued to accelerate globally, and the market realized that while the U.S. economy was only growing at about 2%, it was still growing. As global growth was improving, the risk that 2% growth would fade away seemed more and more unlikely. The market transitioned to embrace the idea that 2% growth, while somewhat below what we had hoped for in the days and weeks following the election, was nevertheless a good environment for stocks.

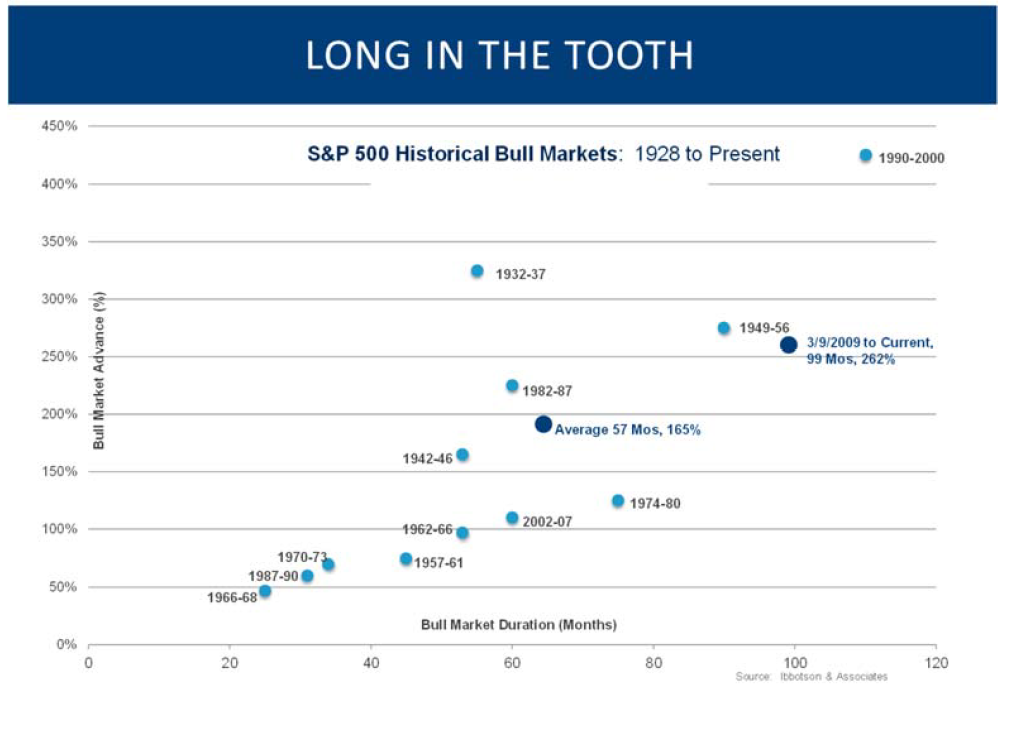

With modest growth came a more modest need for the Fed to tighten monetary policy (more on that later). Without an aggressive Fed policy, it was perceived that the expansion could continue. Already one of the longest expansions in history, there were no signs that this expansion was coming to an end. As growth was accelerating across many parts of the globe, companies continued to report good earnings, and also provided encouraging comments about future prospects.

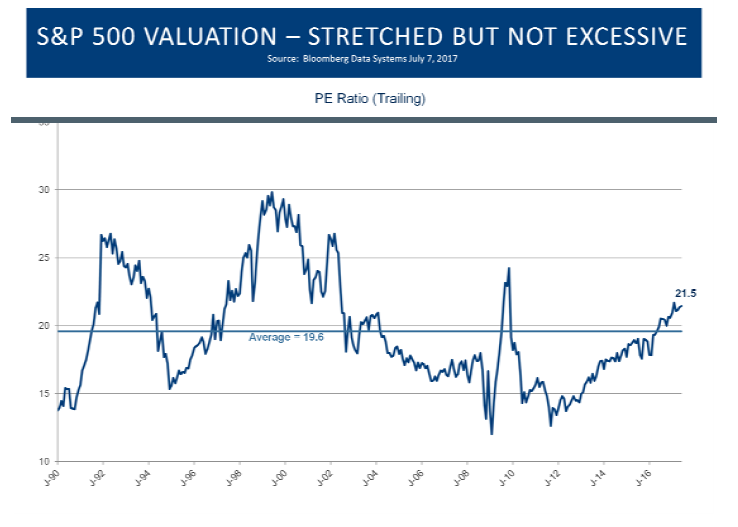

To be sure, by most every measure valuations are a bit stretched. It is important to recognize, however, that valuations are one of the worst short-term indicators. Valuations may help with the forward-looking prospects for returns over the next decade, but they are notoriously abysmal at suggesting the path for returns over the next few years.

Still, despite somewhat elevated valuations, we remain in what one strategist suggested is a “TINA” market. By TINA, he felt that There Is No Alternative to equities. With interest rates moving somewhat higher, with prospects for higher growth in earnings, and with the Fed unlikely to raise interest rates aggressively, it continues to be a TINA market, a market that favors stocks because there is simply no other place to invest.

As we mentioned above, this has been one of the longest expansions in American history. In some respects, this makes sense because we had one of the worst recessions in modern history, and we had a long way to go before economic growth normalized. It also makes sense because the Federal Reserve has been very timid at raising interest rates, fearful that the U.S. recovery was not as yet self-sustaining. It was also fearful that any aggressive move to raise interest rates would tip the U.S. economy back into recession.

We have repeatedly suggested that economic expansions never die of old age (at least not yet). They die following policy mistakes that make monetary policy too tight for the current environment.

The Fed has raised interest rates three times, bringing the Fed Funds rate to between 1% and 1.25%. It is hard to argue that 1% interest rates will be too high for businesses to continue to expand. In fact, when compared with inflation, it could be argued that interest rates are still too low.

How do we determine whether Federal Reserve policy is too tight? Actually it is a pretty straight forward exercise. Other than the Fed Funds rate, all other interest rates are set by the market. Supply combined with Investors’ demand for different investment opportunities set interest rates.

If the government is running large deficits, then the supply of bonds will overwhelm the demand, and prices will fall, pushing interest rates higher. However, whether investors desire short-term investments (say a 2-year treasury) or long-term investments (say a 10 or 30-year treasury) is driven entirely by investor preferences.

When the investment community starts to believe that Federal Reserve policy is too tight, and a recession is on the horizon, investors will favor long-term investments. This is based on the expectations that the Fed will soon stop raising interest rates, and will eventually start to reduce rates to encourage the economy to grow faster again. In this environment, longer investments will appreciate more than shorter investments.

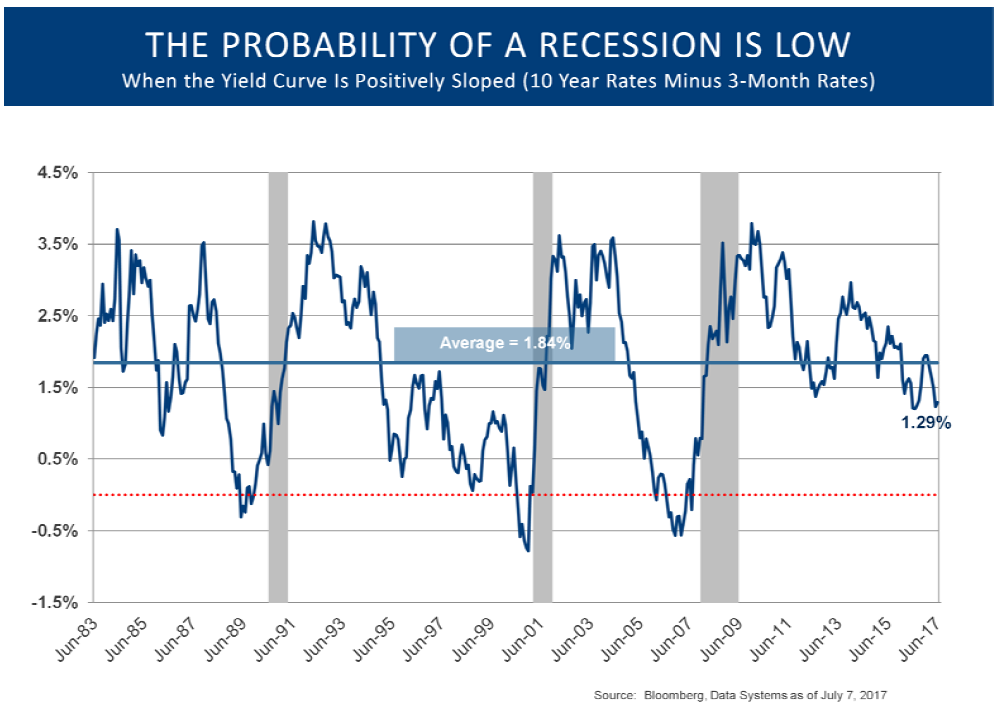

We can compare Fed Funds interest rates with longer-term rates. In a normal environment, longer-term interest rates are above the very short-term Fed Funds rate. However, when Fed Funds rates are perceived by the market as being too high, longer term interest rates can actually fall below the Fed Funds rate. That environment is called an inverted yield curve.

An inverted yield curve suggests the market believes the Fed has been too aggressive at pushing interest rates higher. An inverted yield curve has shown an exceptional ability to forecast when a recession is on the horizon. From the time the yield curve inverts, a recession has generally followed within 3 to 6 quarters.

The yield curve is currently not inverted, and it does not appear that the curve will invert any time soon. That suggests that a recession is not on the horizon for at least the next several quarters.

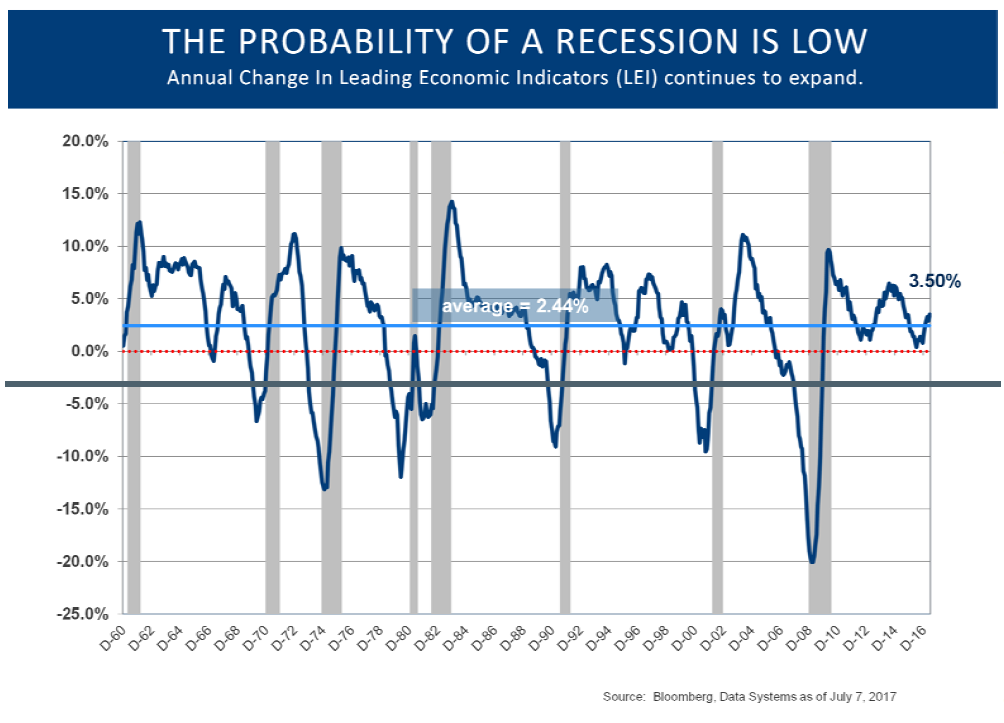

Another one of our best forecasting tools for the timing of the next recession is the U.S. index of leading economic indicators, or “LEI”. The LEI is an index of ten different components. The index contains forward-looking indicators such as initial claims for unemployment insurance, ISM index of new orders, manufacturers orders for consumer goods and capital goods, housing building permits, weekly hours worked in the manufacturing sector, stock prices, consumer expectations, credit spreads, and the shape of the yield curve (inverted or not).

We compare the level of the LEI today with the level of the LEI 12 months prior. If the percent change from a year ago is positive, we can expect the economy to continue to expand. If, on the other hand, the change as compared to a year ago is negative, then we must conclude that the probability of a recession on the horizon has increased. This indicator too has a solid history of forecasting the beginning of a recession roughly 3 to 6 quarters ahead. Like our yield curve analysis, this indicator is not suggesting that a recession is on the horizon for at least several quarters.

In the post World War II era, recessions have been caused by other events, not just by over-zealous Federal Reserve policy-makers. Oil shocks have caused recessions, but oil prices have remained stubbornly low. The technology of hydraulic fracturing, called fracking, has led to a dramatic increase in the oil producing capabilities of the United States. This has changed the balance of power for the OPEC nations and for other oil producers like Russia. While foreign oil producers have agreed to reduce their oil production to help stabilize prices, American oil producers have continued down the learning curve of their newest technologies. Companies that were not profitable with oil prices below $70 or $60 per barrel, now see break-even levels at $40 per barrel. Furthermore, the technology suggests that efficiency will continue to improve, and it may soon be possible for many domestic oil producers to be profitable with oil prices above $30.

Lower oil prices have helped keep inflation below the Fed’s target, and without a geopolitical shock to oil supplies, it does not seem that an oil shock will lead to a recession any time soon.

On the topic of geopolitical risks, we recognize that these are some of the toughest risks to protect portfolios against. By their very nature, exogenous events caused by a dogmatic and dangerous person or group cannot be predicted. A belligerent North Korean leader does not necessarily suggest that geopolitical risks have increased to an unsafe level. We simply have no good way to quantify these risks. While a geopolitical risk that shuts down oil production in the Middle East could easily cause a recession, most geopolitical and terrorist attacks have not had a long-term impact on the stock market. Even 9-11, one of the most heinous terrorist attacks in U.S. history, caused an immediate and disturbing decline in stock market indices. The S&P was actually higher by the end of 2001 than it was on the days before the event. Geopolitical risks are with us and are very hard to predict. The good news is that the impact on long-term corporate profitability has actually been fairly modest.

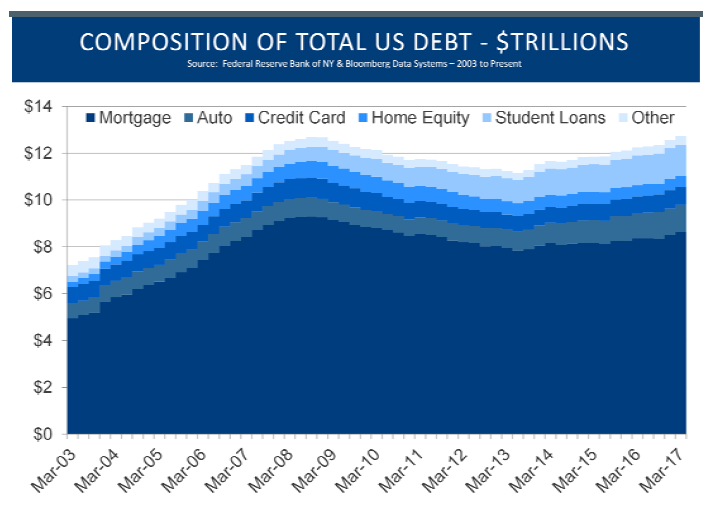

Recessions have also been caused by financial crises, and the Great Recession was one of the most severe since the Great Depression. It is important to recognize that the banking system is on far greater footing than it was in 2006. Every large domestic bank recently passed the Fed’s required stress test, which determines whether the bank will likely survive a series of events that simulate those that led up to the 2008 recession.

It is true there has been an increase in sub-prime auto lending, and it is also true that student loan debt has increased. In the years leading up to the Great Recession, mortgages were not only given to people who could not afford to keep their homes, but these loans were packaged into new-fangled investment vehicles that were virtually all rated AAA by the rating agencies. These highly rated investments were everywhere. They were owned by every high quality bond fund, by every sovereign fund, and by every pension fund. They were ubiquitous. When mortgage bonds started to fail, the ramifications were felt across the economy.

So far, we have not made the same mistake with sub-prime auto loans or with student loans. Some of these loans are packaged into asset-backed investment instruments, but the risk of these loans failing will not lead to the same systemic risks as were witnessed a decade ago. With the balance sheets of most banks and financial institutions in very good shape, it seems unlikely that a financial crisis will precipitate a recession any time soon.

Weak global economic growth has not led to a U.S. recession very often because the U.S. economy is too well-diversified. We do, however, recognize that there is the potential for weak global demand to lead to a recession. As of this writing, most nations seem to be seeing stronger, rather than weaker, economic growth. Our analysis of this data continues to suggest that a recession is not on the horizon.

We have come full circle and believe that one of the largest risks to the longevity of our current recovery is the potential for central bank policy to become too tight. The quotes at the beginning of this newsletter suggest that the age of central bank accommodation may be coming to an end. We do not expect central bank policy to become too tight any time soon, but we do acknowledge that the tone coming from central bankers has changed, and the age of exceptional central bank accommodation may be ending.

We want to take a moment to talk about the proliferation of ETFs and other passively managed investment vehicles. Markets typically go up more than 75% of the time, while declining less than 25% of the time. Investors have embraced these passive investment vehicles, which provide market-like returns with relatively modest costs and fees. These vehicles have been particularly successful in a market environment that has been relatively robust. While we have had some modest corrections, the market has gone up without interruption since 2009 (market returns in 2010 and 2015 were only positive due to dividend yields).

Eventually we expect the economy will stumble, and a recession will ultimately occur. This could lead to a market that may bring stock prices down. In that environment, a more active and tactical manager may have the opportunity to take advantage of market disruptions through either an increased allocation to cash or to an allocation to more defensive sectors of the market. All investment choices have their advantages and disadvantages, and it is important to recognize both the strengths and weaknesses of any strategy employed.

As always, it is important that we know of any changes in your financial situation. Please feel free to call us if you have any questions or comments regarding your investment portfolio.

Bennett Gross CFA, CAIA

President

L&S Advisors, Inc. (“L&S”) is a privately owned corporation headquartered in Los Angeles, CA. L&S was originally founded in 1979 and dissolved in 1996. The two founders, Sy Lippman and Ralph R. Scott, continued managing portfolios together and reformed the corporation in May 2006. The firm registered as an investment advisor with the U.S. Securities and Exchange commission in June 2006. L&S performance results prior to the reformation of the firm were achieved by the portfolio managers at a prior entity and have been linked to the performance history of L&S. The firm is defined as all accounts exclusively managed by L&S from 10/31/2005, as well as accounts managed in conjunction with other, external advisors via the Wells Fargo DMA investment program for the periods 05/02/2014, through the present time.

L&S claims compliance with the Global Investment Performance Standards (GIPS®). L&S has been independently verified by Ashland Partners & Company LLP for the periods October 31, 2005 through December 31, 2015 and ACA Performance Services for the periods January 1, 2016 to December 31, 2016. Upon a request to Sy Lippman at slippman@lsadvisors.com, L&S can provide the L&S Advisors GIPS Annual Disclosure Presentation which provides a GIPS compliant presentation as well as a list of all composite descriptions.

L&S is a registered investment adviser with the U.S. Securities and Exchange Commission (“SEC”) and is notice filed in various states. Any reference to or use of the terms “registered investment adviser” or “registered,” does not imply that L&S or any person associated with L&S has achieved a certain level of skill or training. L&S may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Information in this newsletter is provided for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. Any communications with prospective clients residing in states or international jurisdictions where L&S and its advisory affiliates are not registered or licensed shall be limited so as not to trigger registration or licensing requirements. Opinions expressed herein are subject to change without notice. L&S has exercised reasonable professional care in preparing this information, which has been obtained from sources we believe to be reliable; however, L&S has not independently verified, or attested to, the accuracy or authenticity of the information. L&S shall not be liable to customers or anyone else for the inaccuracy or non-authenticity of the information or for any errors of omission in content regardless of the cause of such inaccuracy, non-authenticity, error, or omission, except to the extent arising from the sole gross negligence of L&S. In no event shall L&S be liable for consequential damages.

The S&P 500 index is a free-float market capitalization weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested and is not available for direct investment. The composition of L&S’ strategies generally differs significantly from the securities that comprise the index due to L&S’ active investment process and other variables. L&S does not, and makes no attempt to, mirror performance of the index in the aggregate, and the volatility of L&S’ strategies may be materially different from that of the referenced indices.

L&S’ current disclosure statement as set forth in ADV 2 of Form ADV as well as our Privacy Notice is available for your review upon request.