January 9, 2020

It’s dangerous to make predictions — especially about the future.

— Yogi Berra

As a young boy, I remember my parents going out one New Years Eve, and as they left they said “see you next year.” I couldn’t believe my parents would abandon me for a whole year, and I started crying. When the concept of New Years Eve was explained to me I felt fine. I still laugh whenever anyone says “see you next year.” Imagine how I would have felt if my parents had said “see you next decade.” I suspect I would have been inconsolable. It is this thought about the end of another decade that got me reflecting about the important changes we have witnessed during the past ten years, and how those events will impact our investment decisions over the coming years. In no particular order, we will review some of the interesting changes that have occurred over the past decade.

Electric Cars—At the turn of the 20th century, electric vehicles were introduced along with cars driven by steam, gasoline, and diesel. In fact, the vehicular land speed record was held by an electric car until 1900. It was not until the first Tesla roadster came out in 2008 that electric cars were once again considered feasible as a transportation alternative.

The first Model S was introduced in 2012. Early adaptors of those cars spoke enthusiastically about a car with enormous torque and very quick acceleration, as well as technology that was the best available at any price. For example, the Tesla knows to open your garage door when you approach your home, and it knows to close the garage door as you drive away.

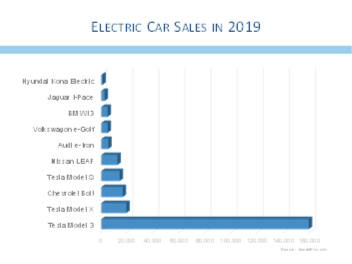

The first Tesla Model 3 rolled off the assembly line in July of 2017, and it was an immediate hit. While the number of competitors offering electric vehicles has increased dramatically, so far no car has been able to unseat the Model 3 as the best selling electric car. Three of the top four electric models sold are all made by Tesla, and the Model 3 sells almost ten times as often as the best-selling non-Tesla electric model (the Chevrolet Bolt).

Some of the capabilities of the Tesla are setting the tone for what automotive technology will offer in other vehicles as we look ahead to the new decade. To begin, the Tesla updates its software via your in-home wifi. This means that the newest features available are not just available on the newest models, but your existing car is also updated to the most modern standards and capabilities. Older Tesla cars are not becoming technologically obsolete. This suggests that older cars are unlikely to depreciate quite as much since the difference between a used car and a new one is much smaller.

Cruise control has been around for decades, but Tesla’s capabilities have set the bar for the car’s ability to maintain speed or a safe distance behind the car ahead. Their technology can keep the car in the middle of the lane and can make steering adjustments as roads curve. This is not an extra feature but is standard on all of their cars. For a princely sum (although much less than the cost of a chauffeur), Tesla also offers self-driving capabilities where the system can make turns, take freeway offramps, and deliver you safely to your destination.

Safety features are big sellers for new cars, and the technology required to keep drivers and passengers safe will continue to expand. It was more than 10 years ago when BMW reported that the cost of computer chips in its 7 Series cars exceeded the cost of steel in those same vehicles.

While electric cars only represent 2% of car sales, some futurists have suggested that a child born today will never own an internal combustion engine car. Perhaps nostalgia will encourage owning and collecting cars that have gasoline engines, but the reality is that companies making parts for internal combustion engines are likely to see the market for their products decline over the coming years. In contrast, companies that make the components for self-driving capabilities, including the newest safety features, will continue to see demand for their products increase. These companies represent an exciting investment opportunity providing, of course, the ability to identify winners along the way.

Cord Cutting—No one has ever said they love their cable company. The “Cable Guy” has become a derogatory moniker that suggests a company that does not care about its customers. While Netflix started as a DVD rental service, it started streaming movies in 2007, and in 2013 it created the first must-watch streaming series—”House of Cards.” “House of Cards” was so popular that it drove millions to subscribe to Netflix. Netflix now represents about 15% of all internet activity.

Cord Cutting suggested that viewers could ditch their cable-tv subscriptions and watch great shows without that monthly service charge that included so many channels that did not provide content that viewers really cared about. Why are

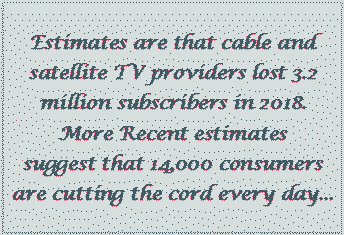

customers paying for ESPN or Discovery or Hallmark when they never watch those channels? Estimates are that cable and satellite TV providers lost 3.2 million subscribers in 2018. More recent estimates suggest that 14,000 consumers are cutting the cord every day. Just as millennial consumers will never have a land-line home phone service, many of them may never have a cable-tv subscription. TV viewing has changed, perhaps forever.

Many content providers have embraced the “House of Cards” model and have produced series that they hope will generate millions of subscribers. HBO has produced “Game of Thrones,” Hulu has “The Handmaid’s Tale,” DisneyPlus has “The Mandalorian,” Apple TV+ has “The Morning Show,” AmazonPrime offers “Fleabag,” and on and on. The problem is that once you have subscribed to four or five different streaming services, you could be paying as much for your streaming services as you were paying for cable.

DisneyPlus announced they have more than ten million subscribers about a month after launching. It took HBO nearly three years to garner a similar number of subscribers. At $7 per month, ten million subscribers generate about $800 million of revenue for Disney. Certainly not chump change, but does it really move the needle for a company that generates nearly $70 billion in revenue per year?

It is interesting to try to determine which companies will benefit from cord cutting. One group of obvious winners are the companies that provide internet connectivity into our homes. Without a robust internet connection, streaming devolves into a jumpy annoying mess and encourages viewers to upgrade their internet service. Can anyone say gigabit speed?

The content providers are a different story. Netflix spends a fortune creating its unique offerings, and, like fashion, tv shows can fall from popularity. Can anyone say they actually watched the last season of “House of Cards?” It is hard to measure the return on investment from a particular show, especially when content providers may produce hits along with several misses. Perhaps these companies need to be evaluated like motion picture producers—able to create some blockbusters along with some perfectly average offerings. Further, the increasing number of content producers suggests a competitive field that could make it difficult for anyone to monetize their investments. Picking winners in cord-cutting may be a difficult, but worthwhile task.

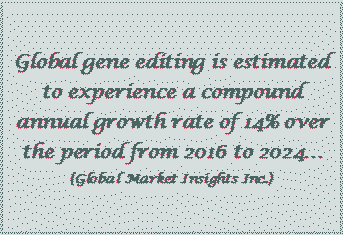

Genetic Editing—The human genome was first sequenced in 2003 after 13 years of work that cost more than $1 billion. Now a basic genetic make-up can be determined by sending a test tube of saliva and less than $100 dollars to one of several providers. More importantly, genetic editing is being focused on chronic and deadly diseases. Imagine altering the genetic make-up of the AIDs virus so that it only attacks cancer cells.

Welcome to the new era of drug discovery. Drugs will be created to treat an ailment of an individual patient. Viruses will be weaponized to treat rather than cause diseases. This is an area that represents so much promise and the potential to change the world for the better. Investment opportunities abound. Some companies will create the processes for altering genes. Other companies will produce the tools necessary for scientists to understand and change a genetic makeup. Still others will be fortunate enough to manufacture treatments that save and extend lives.

Picking winners will be incredibly difficult. Promising new therapies will ultimately fail their phase three trials. Drug side effects will be intolerable. Further study will be required, but will ultimately be fruitful and lead to new treatments. Life expectancies will continue to expand, and that may create investment opportunities as well. Identifying winners early will be incredibly difficult, and will take tremendous effort and some phenomenally good luck, but have the potential to be hugely profitable. It is a rare time in human existence when we have the opportunity to participate in such a life-changing outcome.

The Decline of Globalism—In June of 2016, the British voted to leave the European Union. The Union, taken together, is the largest economy in the world, bigger than the United States or China. Why would anyone want to leave the most successful economic union of all times? The simple answer is that many people felt the sacrifices being made to remain a member were simply no longer worthwhile. Following three years of struggle, the British recently voted to affirm their decision to leave the European Union. Many issues remain unsolved, but the decision to leave the EU suggests the decline of globalism.

Most economists believe that globalization creates more winners than losers. While that may be true, the reality is that some participants will suffer and find themselves on the short end of the globalization trade-off.

In November of 2016, the election of Donald Trump represented another attack on the idea that the benefits of globalization are worthwhile. Workers who suffered as their jobs were shipped overseas voted to elect a candidate they hoped would stem that job loss, and perhaps even reverse the trend.

If economists are right that globalization creates a net gain for the world, then it is likely that global economic growth may slow in the coming decade. That is not to say that investors should shun companies that do business globally. It does suggest that companies may find growth by focusing on more domestic opportunities. Perhaps giant multi-national corporations will struggle to grow while other companies may benefit from markets that favor domestic producers. This may not be all bad for investors.

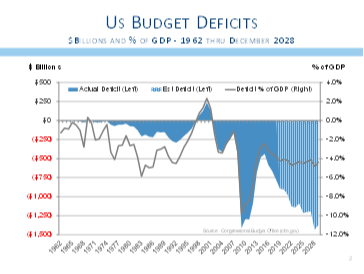

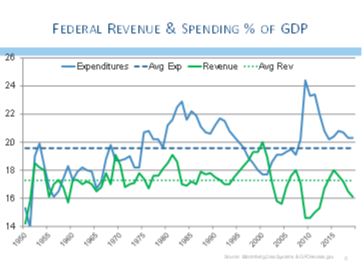

The End of Fiscal Responsibility—English economist John Maynard Keynes argued that one of the roles of government is to run deficits when economic growth is lagging so that government spending fills some of the gap. He also suggested the corollary to deficit spending was to run a surplus when the economy was strong so as to save some funds for a rainy day. Keynesian economics never suggested that deficit spending should occur year in and year out.

One of the key accomplishments of the first Trump administration was a tax cut that made U.S. corporate taxes more competitive on the global stage. However, that tax cut also swelled federal deficits as tax collections dwindled. The idea was that lower taxes would encourage companies to invest in growth opportunities, and accelerating growth would offset any revenue decline from lower tax rates.

Many companies have invested some of the proceeds from lower tax rates into dividend increases and share buybacks, but little has been invested in capital improvements and new plants and equipment. Perhaps the uncertainty over the trade war has caused companies to postpone any new expansion, but so far the reality is that deficits have expanded and growth has not picked up sufficiently to provide an offset.

Neither party has embraced fiscal conservatism, and that is a shame. The United States is running trillion dollar deficits while the economic expansion continues uninterrupted. In fact, this is the longest economic expansion in history, and the decade that just ended was the only decade since the Civil War that did not include a recession. It is unclear why such enormous deficits are warranted. It is even more unclear why no one is suggesting this is a bad idea.

There are proponents of a new economic thesis that argues deficits are not bad. This new thought process is called Modern Monetary Theory (MMT), and it looks at places like Japan that have run huge deficits and have accumulated ginormous outstanding debt as compared with their GDP (Gross Domestic Product). Despite these profligacies, inflation has not be ignited. The MMT theory maintains that deficit spending is acceptable unless it starts to create inflation.

We suspect that Nobel prize-winning economist Milton Friedman would be spinning in his grave. Friedman was famous for saying “inflation is everywhere and always a monetary phenomenon.” His belief was that deficit spending and excessive monetary supply creation would lead to inflation without fail. We do not have the benefit of Friedman’s thinking to help explain current dynamics, but we do worry that uncontrolled deficits will have deleterious effects.

How to invest in a world of unending federal deficits is an interesting question. Should inflation pick up, investors would benefit from adding exposure to materials and commodities. While growth might appear robust due to higher revenue that is driven by inflated prices, the reality is that inflation may also lead to slower growth after the effects of inflation. In a slower growth economy, it might make sense to own companies that produce products that are necessities or are relatively price insensitive. The worry is that higher inflation and slower growth, called stagflation, will create a difficult investment environment.

ESG—Environmental, Social, and Governance — Investors tend to focus on different factors over time. At one point it was popular to embrace Japanese-style management practices. General Electric used to cull workers every year in a process they called six sigma. Six sigma was also used to help reduce defects on a manufacturing line. Different theories have came into fashion, and currently the greatest attention is given to how a company acts as it relates to it environmental, social and governance policies (ESG). This is not to say that any of these focuses are fads, but only to suggest that investors’ focus tends to change over time.

Environmental issues tend to deal with greenhouse gas emissions. How much emissions does the company produce and has their greenhouse gas production diminished over time? How does this compare with other companies in the industry? For example, energy companies are notoriously high greenhouse producers. Further, the use of their product tends to create additional greenhouse gases. Yet, as an investor, it might be important to know whether a company you are considering investing in actually does a better job at minimizing these pollutants than do other companies in the same business.

Social policies tend to deal with issues such as the percentage of women in the workforce, employee turnover, whether the workers are unionized, and how much time is lost to accidents.

Governance policies tend to deal with the makeup of the highest levels of management including how independent the board of directors is. How many women are on the board, how involved the board is, and whether the CEO and the Chair of the board are one and the same?

All of these criteria tend to provide some information about the priorities of management, and whether its focus is solely to benefit shareholders, or whether it considers its role in its community and its impact on other stakeholders. The CFA Institute (keepers of the Chartered Financial Analyst credential) recently completed a study that suggested companies with better ESG ratings also tended to provide higher returns to shareholders. With this in mind, the CFA institute suggested that a financial analyst who did not consider ESG factors in their analysis was missing an important component in the evaluation of a company.

At L&S Advisors we have already included ESG criteria into most of our screens used to identify potential investment candidates. Further, we believe these criteria will only increase in importance as we seek to evaluate attractive investment alternatives in the years to come. Companies that strive to be good citizens, that are concerned with the potential for mankind to alter the planet’s climate, and that try to care for its workers are likely to be superior investments to those companies that do not seek to be good corporate citizens.

There were many other cultural phenomena that occurred during the past decade: Apple introduced the first iPad and the first wearable computer the Apple Watch. The #MeToo movement took off, as did Black Lives Matter and Occupy Wall Street. Fidget spinners came and went as did the solar eclipse. Gangnam Style became the most-watched video ever. There were two Royal weddings. U.S. citizens elected the most diverse House of Representatives in history. The President was impeached for only the fourth time in American history. The Supreme Court approved same-sex marriage while gun control laws remained off limits, despite shootings at Sandy Hook, Parkland, Aurora Colorado, and Las Vegas. The Pope resigned for the first time in nearly 600 years.

It has been quite an interesting decade. Some of these things will have important investment implications while others will pass like the fads they are. We will continue to try to determine which events will create themes that will provide investment opportunities well into the next decade.

As always, it is important that we know of any changes in your financial situation. Please feel free to call us if you have any questions or comments regarding your investment portfolio.

Bennett Gross CFA, CAIA

President

Disclosure

L&S Advisors, Inc. (“L&S”) is a privately owned corporation headquartered in Los Angeles, CA. L&S was originally founded in 1979 and dissolved in 1996. The two founders, Sy Lippman and Ralph R. Scott, continued managing portfolios together and reformed the corporation in May 2006. The firm registered as an investment adviser with the U.S. Securities and Exchange commission in June 2006. L&S performance results prior to the reformation of the firm were achieved by the portfolio managers at a prior entity and have been linked to the performance history of L&S. The firm is defined as all accounts exclusively managed by L&S from 10/31/2005, as well as accounts managed in conjunction with other, external advisors via the Wells Fargo DMA investment program for the periods 05/02/2014, through the present time.

L&S claims compliance with the Global Investment Performance Standards (GIPS®). L&S has been independently verified by Ashland Partners & Company LLP for the periods October 31, 2005 through December 31, 2015 and ACA Performance Services for the periods January 1, 2016 to December 31, 2018. Upon a request to Sy Lippman at slippman@lsadvisors.com, L&S can provide the L&S Advisors GIPS Annual Disclosure Presentation which provides a GIPS compliant presentation as well as a list of all composite descriptions.

L&S is a registered investment adviser with the U.S. Securities and Exchange Commission (“SEC”) and is notice filed in various states. Any reference to or use of the terms “registered investment adviser” or “registered,” does not imply that L&S or any person associated with L&S has achieved a certain level of skill or training. L&S may only transact business or render personalized investment advice in those states and international jurisdictions where we are registered, notice filed, or where we qualify for an exemption or exclusion from registration requirements. Information in this newsletter is provided for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. Any communications with prospective clients residing in states or international jurisdictions where L&S and its advisory affiliates are not registered or licensed shall be limited so as not to trigger registration or licensing requirements. Opinions expressed herein are subject to change without notice. L&S has exercised reasonable professional care in preparing this information, which has been obtained from sources we believe to be reliable; however, L&S has not independently verified, or attested to, the accuracy or authenticity of the information. L&S shall not be liable to customers or anyone else for the inaccuracy or non-authenticity of the information or for any errors of omission in content regardless of the cause of such inaccuracy, non-authenticity, error, or omission, except to the extent arising from the sole gross negligence of L&S. In no event shall L&S be liable for consequential damages.

The S&P 500 index is a free-float market capitalization weighted index of 500 of the largest U.S. companies. The index is calculated on a total return basis with dividends reinvested and is not available for direct investment. The composition of L&S’ strategies generally differs significantly from the securities that comprise the index due to L&S’ active investment process and other variables. L&S does not, and makes no attempt to, mirror performance of the index in the aggregate, and the volatility of L&S’ strategies may be materially different from that of the referenced indices.

L&S’ current disclosure statement as set forth in ADV 2 of Form ADV as well as our Privacy Notice is available for your review upon request.